Essential Guide: ACV vs RCV Roof Insurance

Why “ACV vs RCV roof insurance” decides your check size

If you are filing a storm claim, the first question that shapes your payout is ACV vs RCV roof insurance. ACV pays today’s value after depreciation. RCV pays the current cost to replace. Understanding this difference, plus when Ordinance & Law (code-upgrade) coverage applies, can prevent delays and help you plan cash flow. Homeowners also ask, “Does insurance cover code upgrades?” The answer depends on whether your policy includes building-code coverage, sometimes listed as O&L coverage for roof replacement. For broader context on homeowners coverage and claims, see the Insurance Information Institute

Resource: See how CarbonBlack approaches claim education at CarbonBlack.

ACV vs RCV Roof Insurance: What each one really means

ACV (Actual Cash Value)

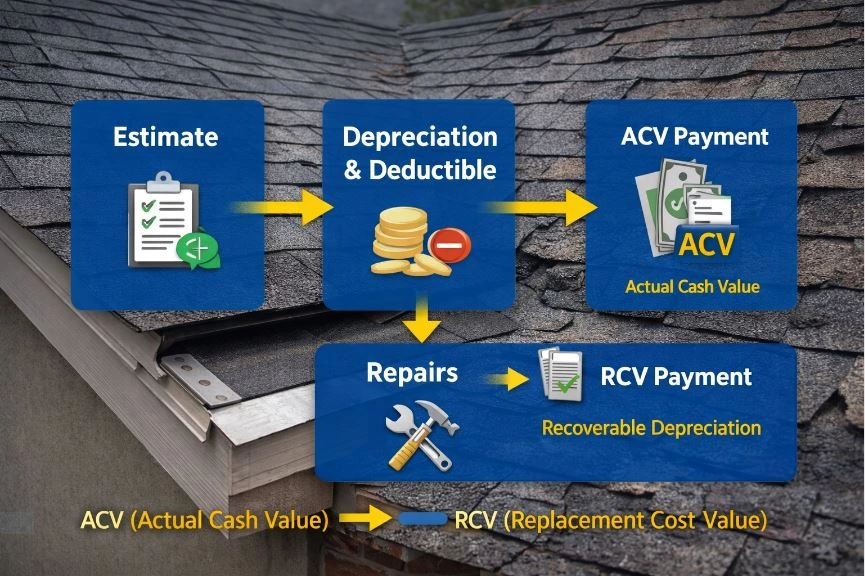

In ACV vs RCV roof insurance, ACV pays the replacement cost minus depreciation.

- What it covers: Replacement cost minus depreciation.

- When you get paid: Typically one check after the adjuster’s estimate, minus your deductible.

- Upside: Lower premiums in many cases.

- Tradeoff: You shoulder the gap between depreciated value and full replacement cost.

RCV (Replacement Cost Value)

- What it covers: The full cost to replace with like kind and quality at today’s prices.

- When you get paid: Usually in two parts: initial ACV, then recoverable depreciation (the “holdback”) after approved proof of completion.

- Upside: Aligns payout with real market prices to restore your roof.

- Tradeoff: Often higher premiums, extra documentation, lender endorsements.

Internal read: Insurance Claim Assistance and Resilient Roofing Solutions.

How insurers calculate your roof payout (with simple math)

Step 1: Determine Replacement Cost

- Labor + materials + waste + accessories + tax = Replacement Cost Estimate (RCE)

Step 2: Apply Depreciation (age and condition)

- If your 20-year shingle roof is 10 years old, many carriers apply linear depreciation near 50% as a rough example. Actual schedules vary by policy and condition.

Step 3: Subtract Deductible

- Your policy deductible is taken from the payout, not your contractor’s invoice.

Example side-by-side

Item | ACV Policy | RCV Policy |

Replacement Cost Estimate (RCE) | $15,000 | $15,000 |

Depreciation (example 50%) | -$7,500 | -$7,500 |

ACV (initial payment) | $7,500 | $7,500 |

Deductible (example $2,000) | -$2,000 | -$2,000 |

Initial Check | $5,500 | $5,500 |

Recoverable Depreciation | N/A | $7,500 (released after completion) |

Total Potential Payout | $5,500 | $13,000 |

Note: Mortgage lenders may need to co-endorse checks. See the mortgage section below.

Where Ordinance & Law fits: Code upgrades and “hidden” costs

Even with RCV, new codes can require upgrades, such as drip edge, underlayment, ventilation, or sheathing corrections. That is where Ordinance & Law (O&L) coverage helps.

Code upgrade coverage roof: what it does

- Pays for required building code upgrades, up to your O&L limit.

- Often listed as 10%–50% of Coverage A, or a flat dollar amount. Limits vary.

“Does insurance cover code upgrades?”

- Yes, if your policy includes building code coverage homeowners know as O&L.

- No, if O&L is excluded or the upgrade is not code-mandated for your project.

O&L coverage roof replacement examples

- Drip edge required by current code, but missing on your old roof.

- Decking repairs when code prohibits nailing into damaged boards.

- Ventilation upgrades to satisfy current standards.

Recoverable depreciation and the “holdback” on RCV policies

If you have RCV, the second payment is recoverable depreciation. To release it, insurers usually require:

- Final invoice or proof of cost,

- Photos or a completion certificate,

- Passing inspection where applicable.

If the final approved cost is lower than the estimate, the holdback adjusts accordingly. If your cost is higher than initially approved, your contractor can submit a supplement with documentation.

See also: How to Get Insurance to Pay for Your Roof Replacement and our Insurance Claims Help.

Mortgage checks, endorsements, and fund release

Most homeowner policies list your mortgage company as an additional payee. Expect a two-party check and a loss draft process.

Typical sequence

- Receive initial ACV check payable to you and the lender.

- Endorse through the lender’s loss draft department.

- Lender may release a portion up front, hold the rest until inspections or completion.

- After completion, submit final documents to release remaining funds and, for RCV, the holdback.

When ACV might be enough, and when RCV is worth it

ACV can work if your roof is newer, market replacement costs are stable, or you are comfortable covering depreciation.

RCV is valuable when materials and labor are rising, storms are frequent, or you want the policy to match full replacement costs. Add O&L to avoid footing code-driven surprises.

Explore how we build for durability: Tech-Powered, Storm-Ready Roofs and real projects in the Project Gallery.

Review Your Roof & Policy Side by Side

FAQ

1) What is the main difference between ACV and RCV for roof claims?

ACV pays the depreciated value after age and condition are considered. RCV covers the full replacement cost, usually with a second payment for recoverable depreciation after work is complete.

2) Does insurance cover code upgrades on my roof?

Only if you carry Ordinance & Law coverage. Without O&L, code-required items often become out-of-pocket.

3) How do I get the recoverable depreciation released?

Provide proof of completion, photos, and a final invoice that matches the approved scope. Your insurer may also request an inspection or additional forms.

4) Why is my mortgage company on the insurance check?

Lenders are listed as an additional payee to protect the property’s value. You will need to follow the lender’s loss draft process to endorse and release funds.

5) Is ACV cheaper than RCV for premiums?

Often yes, but many homeowners prefer RCV because it aligns the payout with real replacement costs, especially during inflation or after large storms.

Key Takeaways

- ACV vs RCV roof insurance determines whether you receive depreciated value or full replacement cost.

- Recoverable depreciation is the second payment on RCV claims, released after completion.

- Ordinance & Law coverage answers does insurance cover code upgrades by funding code-required items, up to the limit.

- Mortgage involvement can delay checks; plan for endorsements and inspections.

- Documentation and communication speed approvals and final payouts.